Page 114 - Demo

P. 114

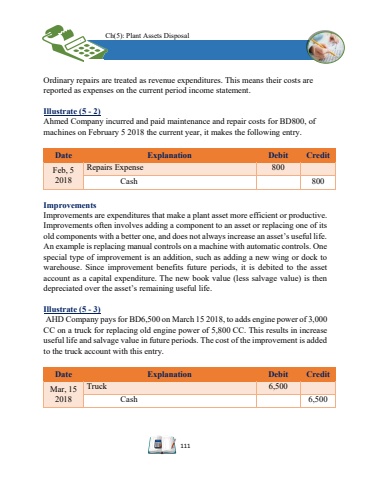

Ch(5): Plant Assets Disposal111Ordinary repairs are treated as revenue expenditures. This means their costs are reported as expenses on the current period income statement.Illustrate (5 -2)Ahmed Company incurred and paid maintenance and repair costsfor BD800,of machines on February 5 2018 thecurrent year, it makes the following entry.DateExplanationDebitCreditFeb,52018Repairs Expense800Cash800ImprovementsImprovements areexpenditures that make a plant asset more efficient or productive. Improvementsoften involves adding a component to an asset or replacing one of its old components with a better one, and does not always increase an asset%u2019s useful life. An example is replacingmanual controls on a machine with automatic controls. One special type of improvement is an addition, such as adding a new wing or dock to warehouse. Since improvement benefits future periods, it is debited to the asset account as a capital expenditure. The new book value (less salvage value) is then depreciated over the asset%u2019sremaining useful life. Illustrate (5 -3)AHD Company paysforBD6,500on March 15 2018,to addsengine power of 3,000 CCon a truckfor replacing old engine power of 5,800 CC. This results in increase useful life and salvage value in future periods. The cost of the improvement is added to the truck account with this entry. DateExplanationDebitCreditMar,152018Truck6,500Cash6,500